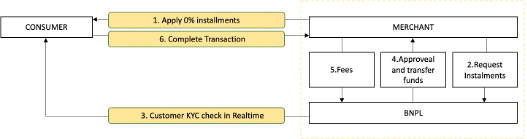

BNPL Technology How does it work?

Experts have been on the lookout onin fintech industry will know that, beyond the bizarre domain of crypto and NFT’s, the matter of the moment right now is “buy now pay later” — or BNPL. For more than a decade the BNPL market has till today, been dominated by the Sweden’s Klarna — Europe’s heavy weight champion of fintech unicorn at a valuation of over $45bn and Australia’s AfterPay, which in August 2021 was acquired by Square for a $29bn.

The key element of BNPL solution is data and not just any data, for precise credit scoring data should be fetched from independent sources then the traditional channels such as behavioural scores, telco information, and open banking to provide real-time understandings of the credit affordability and risk. Accruing data froma wide array of sources at the same time having the ability to swiftly validate and integrate the new source of data, which will contribute in decision accuracy.

The above argument is only voluble if zero hard-coding is likely. Fintech ecosystem is navigating toward prebuilt vendor APIs, in which integration times are seamless. Such integration will limit data access on need bases only, whether in decisioning making process, onboarding process, or performance analysis MIS’s.

BNPL Application design?

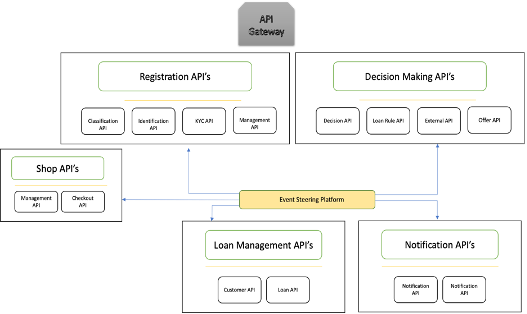

The BNPL architecture requires microservices and eventdriven architecture to enable the different application modules to match features with third-party consumers via APIs, with each API created as a vessel-based microservice. Finally, the APIs are exhibited to external consumers via a gateway through which the authentication and authorization procedure takes place. The application modules are directed by business processes, which are mounted on Business Process Management Engine, besides that each module uses SQL database for transactional and operational purposes. Rational database management system is applied to manage structured data. Data caching is also performed, where applicable. The Next Best Offering component of the Decision-Making Module is built on the basis of ML capabilities. Modules are completely decoupled and interact with each other via the Event Streaming Platform.

What kind of computing BNPL requires?

BNPL providers are always on the excursion to find enhanced, swift methods to assist consumers with or without credit history to increase their book size and revenue opportunities. Leveraging on serverless computing, customers are offered services such as Artificial Intelligence Machine Learning, which redesigns the accuracy and speed of underwriting, in addition to modeling consumer credit risk. Moreover, they can build consistent APIs across countless services that supports fast and seamless integration with third parties and partners.

Due to the decoupled nature of the BNPL with its surrounding Ecosystem the associated services are only aware of the event router, not each other. This means that the services running on the BNPL are interoperable, even though if one service fails, the rest will keep running. The event router acts as an elastic memory that will accommodate surges in workloads.

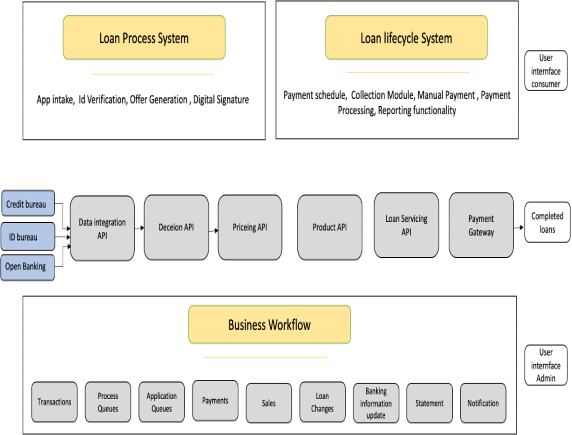

The crucial module of the BNPL ecosystem is the loan processing API, which is used to issue credit facility for the tcustomers and maintain credit account information for billing and processing on the platform. After the credit is confirmed, the credit agreement is digitally created, published, and sent to the borrower and BNPL provider.

Once the loan is originated the BNPL providers would need to underwrite the loan and manage it, as the profitability for BNPL companies depends on several variables:

- Net Take Rate: commission charged to merchants minus payment processing fees that the BNPL provider pays.

- Debt financing cost: corresponds to the interest BNPL providers pay banks for liquidity.

- Debt management cost: credit check costs plus payment collection costs minus late fee payments collected from customers.

- Provision for debt impairment: which represents the weighted average percentage of loans that are not paid back.

The product of the above four variables represent the contribution margin. Startup BNPL providers tend to have a negative contribution margin as losses incurred from debt impairment wipe out any income generated. Hence having adequate Loan management API’s is a key. Loan management system module keeps customers updated on all their payments made via platform. Furthermore, it keeps customers informed via emails and notifications processed by native mobile apps.The loan management module can also be integrated with SMS service providers and mobile network operators to keep users informed about their payment deadlines.

Merchant Onboarding & Management

The main success factor to merchet on onboarding process is automation. A major pain point for BNPL providers is manual data entry, which is carried out multiple times during the traditional onboarding methods. Manual work slows the process down and also introduces inevitable human error. Manual work also adds a significant cost to the process. There are several stages to the process of successfully automating the onboariding of a merchant:

- Prescreening API’s

- Merchant KYC/identity verification API’s.

- Business and operational model analysis.

- Web content analysis.

- Information security compliance.

- Credit risk underwriting.

The key value proposition for BNPL provider is to help merchants boost average order values (AOVs) and acquisition rates, which are both vital revenue drivers. Moreover, BNPL checkouts should be seamless and incorporated into merchant web and mobile sites via APIs that don’t require developer resources.

All this comes at a price, merchant fees 3 times higher then what credit firms card typically charge, BNPL providers aim to drive increased sales conversions and repeat purchases while lowering user acquisition costs. The adaptable nature of APIs has enabled multiple providers to offer BNPL. Since BNPL provider APIs are cloud-based and designed to mix-and-match, it supports adoption virtually or physically. This allows both street side businesses and eCommerce shops alike to offer BNPL services. As those merchants scale, the APIs scale and iterate with them. As new use cases become available, retailers can incorporate those that complement their business models. BNPL can be specified within various parameters —an enticing value made possible by APIs.

Future outlook

Headless commerce is becoming the norm since the adoption of API infrastructure, as it allows a business’s brand to remain at the forefront and reduces disruption to the platform interface during backend updates. These major advantages are wins for users, who can enjoy a continuous brand experience across devices without service interruptions.

Continuous brand experiences and omnichannel touchpoints have become a sticking point for customers. 90% of consumers expect a seamless, omnichannel experience across devices and 73% shop across multiple channels. BNPL APIs fulfils those expectations, enabling the desired experience for shoppers online or in-store. The stress-free nature of integration of BNPL API-based platforms have increased their demand and adoption rates, resulting prosperity thus far and are now catalysing innovation among incumbent players.

Fintech is about innovating financial services to create a seamless and more relevant to the market. The pandemic threw our world into turmoil, but API-based BNPL solutions have provided a new perspective on the formerly unsexy loan, and more importantly, helped people in need take control of their personal finances during an extremely difficult time. Ultimately, isn’t that why we innovate?